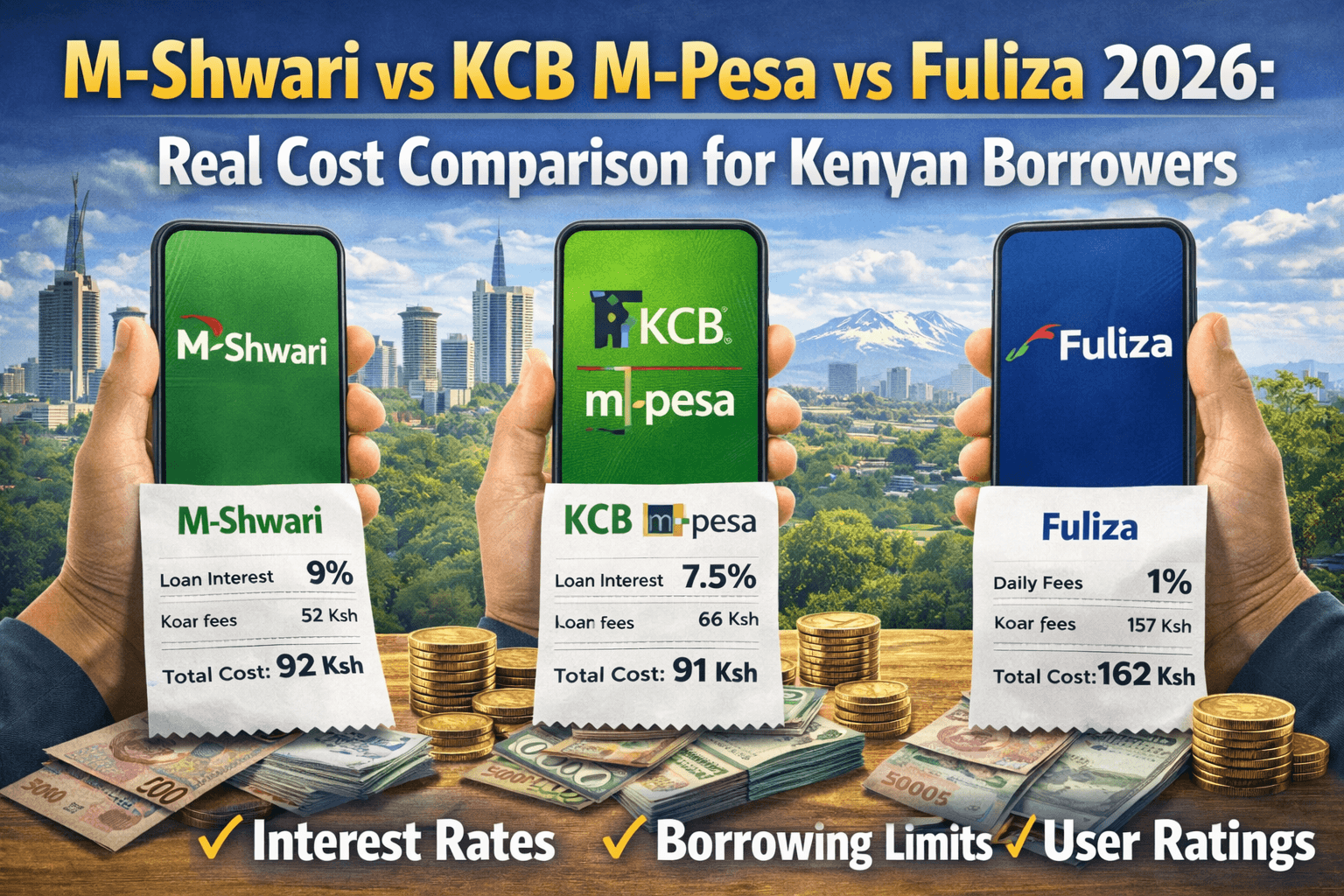

M-Shwari vs KCB M-Pesa vs Fuliza: Which Is Better and Cheapest?

M-Shwari vs KCB M-Pesa vs Fuliza — same Safaricom phone, same KES 1,000 need, three very different costs. Here is the direct answer before anything else:

KCB M-Pesa is cheaper than both M-Shwari and Fuliza at every amount and every duration. The only exception is Fuliza for 1–3 day needs on very small amounts when KCB M-Pesa is not accessible.

| Product | KES 1,000 for 7 days | KES 1,000 for 30 days |

|---|---|---|

| KCB M-Pesa | KES 23 ✅ | KES 50 ✅ |

| M-Shwari | KES 75 | KES 75 |

| Fuliza | KES 90 | KES 320 |

The difference between cheapest and most expensive over 30 days: 540%. Most Kenyans use whichever comes up first on the M-Pesa menu without comparing. This guide fixes that in under five minutes.

⚠️ Rate verification note: KCB M-Pesa fee structures have been updated periodically in 2026. The cost tables in this article are based on an approximately 5% monthly rate. A competitor source published in June 2026 cited a 9.06% facility fee. Verify current KCB M-Pesa rates at kcbgroup.com or by dialling *844#before borrowing. The hierarchy (KCB cheapest, Fuliza most expensive) holds under any realistic rate scenario.

Which Is Better — KCB M-Pesa or M-Shwari?

This is the question most Kenyans are actually asking — and the answer depends on what you mean by “better.”

If better means cheapest: KCB M-Pesa wins at every duration from 1 day to 6 months. For KES 1,000 borrowed for 30 days, KCB M-Pesa costs approximately KES 50 versus M-Shwari’s KES 75.

If better means most predictable: M-Shwari wins. Its flat 7.5% facilitation fee is charged upfront. You know exactly what you owe from day one — KES 1,000 costs KES 75 whether you repay in 1 day or 30 days. No surprises.

If better means most flexible: KCB M-Pesa wins again. It is the only M-Pesa product offering installment repayment terms of 1, 3, or 6 months. M-Shwari requires full repayment within 30 days.

The verdict for most borrowers: Register for KCB M-Pesa via *844# and use it as your primary mobile credit source. Keep M-Shwari as backup for when your KCB limit is insufficient. Avoid Fuliza for anything beyond 3 days.

How Each Product Actually Works

M-Shwari — NCBA Bank via Safaricom

How to access: Dial *334# → M-Shwari → Borrow

Cost structure: A one-time facilitation fee of 7.5% charged upfront on the loan amount. No daily fees. Whether you repay in 1 day or 30 days, you pay the same amount.

Example: KES 1,000 loan = KES 75 fee. Total repayment: KES 1,075.

Key details:

- Loan range: KES 100–50,000 (depending on usage history)

- Term: 30 days. One 30-day extension available at an additional 7.5%

- CRB impact: Reports to all three bureaux. Adverse listing after 90 days non-payment

- Strength: Fixed, predictable cost from day one

- Weakness: Flat fee makes it expensive for short-duration borrowing

KCB M-Pesa — KCB Bank via Safaricom

How to access: Dial *844# to register (one-time), then borrow via the M-Pesa menu

Cost structure: Monthly interest of approximately 4–8% (verify current rate at kcbgroup.com) charged on the outstanding balance only. Repay early and pay less.

Example: KES 1,000 for 1 month at 5% = KES 50 interest. Total repayment: KES 1,050.

Key details:

- Loan range: KES 50–1,000,000 (highest ceiling of any M-Pesa product)

- Terms: 1, 3, or 6 months — the only mobile loan with installment options

- CRB impact: Reports to CRBs. Adverse listing typically after 120 days non-payment

- Strength: Cheapest rate, most flexible repayment terms, highest limits

- Weakness: Requires registration and limit-building period

Fuliza — NCBA Bank via Safaricom

How to access: Enroll once via *334# → Fuliza → Opt In. Activates automatically when your M-Pesa balance is insufficient for a transaction.

Cost structure: A one-time access fee per transaction plus a daily maintenance fee on the outstanding balance every single day it remains unpaid.

Example: KES 1,000 = approximately KES 20 access fee + KES 10 per day outstanding.

Key details:

- Limit: KES 100–70,000 based on M-Pesa history

- Term: No fixed term. Repaid automatically when money enters your M-Pesa

- CRB impact: Outstanding balance reduces M-Shwari limit immediately. CRB listing after 90 days

- Strength: Instant, automatic — completes transactions when your balance falls short

- Weakness: The most expensive option for any duration beyond 3 days

The Full Cost Comparison — Real Shillings for Every Amount

Screenshot these tables. Use them every time you need to borrow.

Assumptions: M-Shwari 7.5% flat fee. KCB M-Pesa approximately 5% monthly on balance (verify current rate). Fuliza 2026 fee schedule — verify at safaricom.co.ke before borrowing.

Borrowing KES 500

| Product | 1 Day | 3 Days | 7 Days | 14 Days | 30 Days |

|---|---|---|---|---|---|

| M-Shwari | KES 38 | KES 38 | KES 38 | KES 38 | KES 38 |

| KCB M-Pesa | KES 2 ✅ | KES 6 ✅ | KES 12 ✅ | KES 23 ✅ | KES 25 ✅ |

| Fuliza | KES 15 | KES 25 | KES 45 | KES 80 | KES 160 |

Borrowing KES 1,000

| Product | 1 Day | 3 Days | 7 Days | 14 Days | 30 Days |

|---|---|---|---|---|---|

| M-Shwari | KES 75 | KES 75 | KES 75 | KES 75 | KES 75 |

| KCB M-Pesa | KES 4 ✅ | KES 12 ✅ | KES 23 ✅ | KES 47 ✅ | KES 50 ✅ |

| Fuliza | KES 30 | KES 50 | KES 90 | KES 160 | KES 320 |

Borrowing KES 2,000

| Product | 1 Day | 3 Days | 7 Days | 14 Days | 30 Days |

|---|---|---|---|---|---|

| M-Shwari | KES 150 | KES 150 | KES 150 | KES 150 | KES 150 |

| KCB M-Pesa | KES 7 ✅ | KES 22 ✅ | KES 47 ✅ | KES 93 ✅ | KES 100 ✅ |

| Fuliza | KES 50 | KES 90 | KES 170 | KES 310 | KES 630 |

Borrowing KES 5,000

| Product | 1 Day | 3 Days | 7 Days | 14 Days | 30 Days |

|---|---|---|---|---|---|

| M-Shwari | KES 375 | KES 375 | KES 375 | KES 375 | KES 375 |

| KCB M-Pesa | KES 17 ✅ | KES 55 ✅ | KES 115 ✅ | KES 233 ✅ | KES 250 ✅ |

| Fuliza | KES 80 | KES 140 | KES 260 | KES 470 | KES 950 |

Borrowing KES 10,000

| Product | 1 Day | 3 Days | 7 Days | 14 Days | 30 Days |

|---|---|---|---|---|---|

| M-Shwari | KES 750 | KES 750 | KES 750 | KES 750 | KES 750 |

| KCB M-Pesa | KES 33 ✅ | KES 110 ✅ | KES 230 ✅ | KES 467 ✅ | KES 500 ✅ |

| Fuliza | KES 150 | KES 250 | KES 450 | KES 850 | KES 1,600 |

The pattern: KCB M-Pesa wins at every amount and every duration. M-Shwari beats Fuliza from day 7 onwards. Fuliza is only justifiable for 1–3 days on very small amounts when KCB M-Pesa is inaccessible.

KCB M-Pesa vs M-Shwari Savings — Which Should You Use?

Both products include a savings component alongside their loan facilities. Here is how they compare for saving rather than borrowing:

M-Shwari savings:

- Earns approximately 2–4% per annum on your balance

- Accessible same-day — no lock-up required unless you choose the lock savings option

- Lock savings earns higher interest (verify current rate via *334#)

- Keeps money separate from your main M-Pesa balance — reduces impulse spending

- Minimum: KES 1

KCB M-Pesa savings:

- Interest rates vary — verify current rate via *844#

- Accessible through the KCB M-Pesa interface

- Saving consistently in KCB M-Pesa also helps grow your loan limit

The better savings choice for most Kenyans: Neither. Both pay significantly below the 10–13% annual yields available from CMA-regulated Money Market Funds accessible via M-Pesa Paybill. Use M-Shwari or KCB savings for your immediate emergency buffer (money you might need same-day), and move anything you can leave for 2–3 days to a money market fund for meaningfully better returns.

When to Use Each Product — The Simple Decision Rule

Use KCB M-Pesa when:

- You are already registered (dial *844# now even if you don’t need it — your limit starts growing immediately)

- Any amount from KES 500 to KES 50,000

- Any duration from 1 day to 6 months

- You want installment repayment rather than a lump sum

- You want the lowest possible cost — it wins at every amount and duration

Use M-Shwari when:

- KCB M-Pesa is inaccessible or your limit is too low

- You need 14–30 days to repay and want a fixed, known cost from day one

- Amount is under KES 20,000

- You prefer a flat fee over a daily accruing structure

Use Fuliza when:

- You need money for 1–3 days maximum and will definitely repay immediately

- The amount is small — under KES 500

- You need to complete a transaction right now with no time to access another product

The only scenario where Fuliza is genuinely justified: You need KES 300 for a matatu, you have money arriving tomorrow, and you cannot wait. Cost: KES 15. Worth the convenience.

Fuliza for KES 2,000 over 30 days = KES 630. M-Shwari for the same = KES 150. You waste KES 480 by defaulting to Fuliza.

Use none of them when:

- You are borrowing regularly at month-end — this is a budgeting problem, not a credit need

- The Hustler Fund covers your need — at 8% per annum it costs KES 6.58 to borrow KES 1,000 for 30 days versus M-Shwari’s KES 75

- You have SACCO access — emergency loans at 12% annual are 87% cheaper than M-Shwari

- You have savings — using them costs zero

Hustler Fund vs M-Shwari vs KCB M-Pesa — The Cheapest Option Overall

Before using any M-Pesa loan product, check your Hustler Fund limit via *254#. The government-backed Hustler Fund at 8% per annum is dramatically cheaper than all three M-Pesa products.

| Lender | Cost for KES 1,000 / 30 days | Annualised rate |

|---|---|---|

| Hustler Fund | KES 6.58 ✅ | 8% p.a. |

| KCB M-Pesa | KES 50 | ~60% p.a. |

| M-Shwari | KES 75 | ~90% p.a. |

| Fuliza | KES 320 | ~365% p.a. |

KES 6.58 versus KES 75 means the Hustler Fund saves you 91% on the same borrowing need. Always check *254# first.

Real Scenarios — Which to Choose

Scenario 1: Emergency hospital deposit — KES 5,000, repay in 7 days

- KCB M-Pesa: KES 115 ✅ Winner

- Fuliza: KES 260

- M-Shwari: KES 375

Scenario 2: Rent arrears — KES 2,000, repay in 21 days

- KCB M-Pesa: KES 70 ✅ Winner

- M-Shwari: KES 150

- Fuliza: KES 450

Scenario 3: Airtime — KES 100, repay tomorrow

- KCB M-Pesa: KES 1 ✅ Winner

- Fuliza: KES 7 (acceptable if KCB not accessible)

- M-Shwari: Minimum loan often KES 500 — overkill for KES 100

Scenario 4: School fees — KES 10,000, repay over 3 months

- KCB M-Pesa: KES 500–750 in installments ✅ Winner — only product with installment terms

- M-Shwari: KES 750 due in 30 days — too short for this need

- Fuliza: KES 4,500+ over 90 days — never use for this

- Better alternative: SACCO emergency loan at 12% annual = KES 300 total

How All Three Affect Your CRB Record

All three products report to Kenya’s three licensed Credit Reference Bureaux — TransUnion, Metropol, and Creditinfo. There is no consequence-free mobile lending on the Safaricom platform.

| Product | Warning Period | CRB Listing | Duration |

|---|---|---|---|

| M-Shwari | 30–60 days | Day 90+ | 5 years from settlement |

| KCB M-Pesa | 30–90 days | Day 120+ | 5 years from settlement |

| Fuliza | 30–60 days | Day 90+ | 5 years from settlement |

Fuliza’s hidden danger: An outstanding Fuliza balance reduces your M-Shwari limit immediately — before any formal CRB listing. Even KES 200 sitting unpaid quietly shrinks your access to all Safaricom credit products while you are unaware.

The combined default scenario: Defaulting on all three simultaneously creates three separate adverse CRB entries. KES 9,500 in total unpaid mobile loans can block access to bank loans, SACCO loans, formal employment in financial roles, and all mobile credit for five or more years.

Repay Fuliza the moment money arrives. It accumulates silently and damages your credit position before you notice.

How Repayment Behaviour Grows Your Limits

Consistent on-time repayment across all three products builds your credit ceiling progressively:

| Month | M-Shwari | KCB M-Pesa | Fuliza |

|---|---|---|---|

| Month 1 | KES 1,000 | KES 500 (just registered) | KES 500 |

| Month 3 | KES 3,000 | KES 2,000 | KES 1,500 |

| Month 6 | KES 10,000 | KES 10,000 | KES 3,000 |

| Month 12 | KES 25,000 | KES 30,000 | KES 8,000 |

Total credit access after 12 months of responsible use: over KES 60,000 across all three products. One missed payment starts collapsing all three simultaneously.

What Borrowing KES 2,000 Monthly Costs You Annually

If you borrow KES 2,000 every month and repay in 30 days, here is what you are paying per year:

| Product | Monthly cost | Annual cost |

|---|---|---|

| Hustler Fund | KES 13 | KES 156 |

| KCB M-Pesa | KES 100 | KES 1,200 |

| M-Shwari | KES 150 | KES 1,800 |

| Fuliza | KES 630 | KES 7,560 |

A Fuliza user paying KES 7,560 per year on a KES 2,000 monthly borrowing habit could instead join a SACCO at KES 500/month and have KES 6,000 in shares after one year — building wealth rather than paying fees.

Your Action Plan — Three Things to Do

Today: Register for KCB M-Pesa via *844# — takes 5 minutes and your limit starts growing immediately even before you need to borrow.

This week: Check your Hustler Fund limit via *254#. Know what you can access before you next need emergency credit.

This month: Start a KES 500/month M-Pesa Goal Savings emergency fund via *234# → M-Shwari → Save. After 6 months you have KES 3,000 available at zero borrowing cost when an emergency arrives.

Frequently Asked Questions

Which is better — M-Shwari or KCB M-Pesa? KCB M-Pesa is better by every measurable metric — it is cheaper (KES 50 versus KES 75 for KES 1,000 over 30 days), offers installment repayment terms, has a higher loan ceiling, and reports to CRBs with a longer grace period (120 days versus 90). The only reason to use M-Shwari over KCB M-Pesa is if your KCB limit is too low or you haven’t registered yet. Dial *844# to register for KCB M-Pesa now.

Which is cheaper — Fuliza or M-Shwari? M-Shwari is cheaper for anything over 7 days. KES 1,000 for 30 days costs KES 75 on M-Shwari versus KES 320 on Fuliza. Fuliza is only cheaper for 1–3 day needs on small amounts — and even then, KCB M-Pesa beats both.

What is the M-Shwari interest rate in 2026? M-Shwari charges a one-time 7.5% facilitation fee on the loan amount — not a daily rate. KES 1,000 costs KES 75 whether you repay in 1 day or 30 days. Expressed as an annualised rate, 7.5% per 30 days equals approximately 90% per annum.

What is the KCB M-Pesa USSD code? Dial *844# to register for KCB M-Pesa and access your loan account. Registration is one-time. After registering, you can also access KCB M-Pesa through the main M-Pesa menu.

How do I increase my KCB M-Pesa limit? Register via *844#, borrow a small amount, repay early, repeat. KCB’s system rewards consistent on-time repayment with progressive limit increases. Also save small amounts in your KCB M-Pesa account — this signals active customer behaviour and accelerates limit growth. Three on-time repayments typically push limits from KES 500 to KES 2,000–5,000.

Can I use M-Shwari and Fuliza at the same time? Yes — both can be active simultaneously. However, an outstanding Fuliza balance reduces your M-Shwari limit. Any money entering your M-Pesa automatically repays Fuliza before you can use it for M-Shwari repayment. Best practice: clear Fuliza completely before taking a new M-Shwari loan.

Does Fuliza affect my CRB record? Yes. Fuliza outstanding for 90+ days results in an adverse CRB listing. Even before that, persistent non-payment reduces your limits across all Safaricom credit products immediately. Repay Fuliza the moment income arrives.

Which mobile loan has the lowest interest in Kenya? The Hustler Fund at 8% per annum (dial *254#) is the cheapest formal loan available to most Kenyans. Among M-Pesa products: KCB M-Pesa (~60% annualised) is cheapest, followed by M-Shwari (~90% annualised), then Fuliza (~365% annualised over 30 days).

Related Guides

- Hustler Fund Kenya 2026 — 8% government loan, full guide

- Best SACCOs Kenya 2026 — 12% emergency loans for members

- CRB Kenya 2026 — check your credit record, dispute errors, clear listings

- How to Save Money in Kenya 2026 — emergency fund strategy to stop borrowing

- Best Money Market Funds Kenya 2026 — earn 10–13% on savings instead of paying 90%

- How to Budget in Kenya 2026 — fix the root cause of month-end borrowing

Rates verified from NCBA, KCB, and Safaricom official sources as of March 2026. KCB M-Pesa rates subject to change — verify current rates at kcbgroup.com or via *844# before borrowing. Cost tables use approximately 5% monthly KCB rate; a June 2026 competitor source cited 9.06% — verify before acting on these figures. Last updated July 2026. This article is for educational purposes only and does not constitute financial advice.