NSSF Year 4 Rates 2026: How Much More Are You Paying From February?

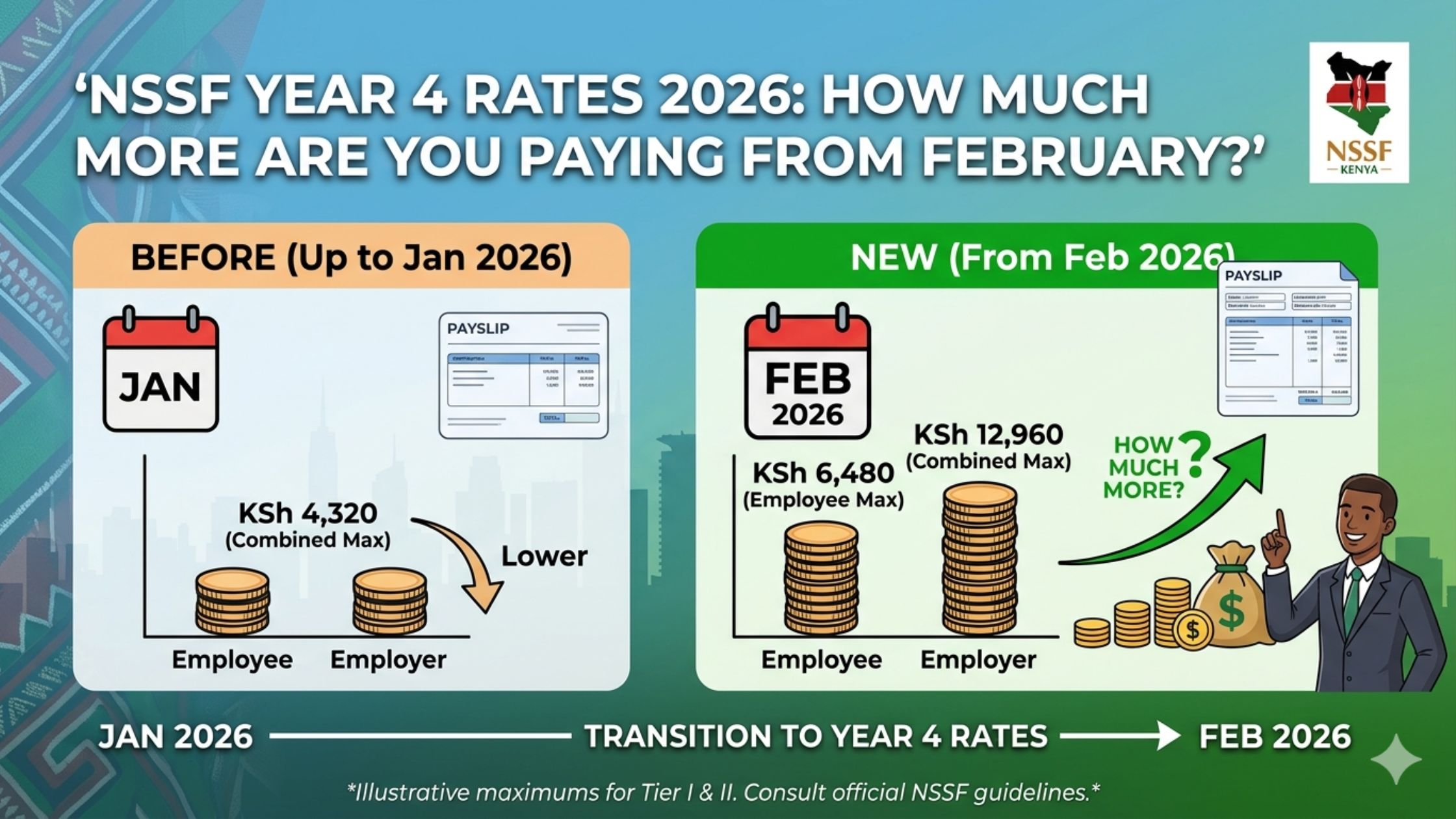

NSSF Year 4 rates in Kenya took effect in February 2026, and millions of Kenyans noticed a quiet but significant reduction in their take-home pay. The Upper Earnings Limit increased to KES 108,000, raising the maximum employee NSSF contribution to KES 6,480 per month — up from the Year 3 figure — and employers are now matching that contribution shilling for shilling.

If your payslip looked different in February and you didn’t know why, this article explains exactly what changed, how much you are now paying, and whether you are getting value for it.

What Is NSSF and Why Do the Rates Keep Changing?

The National Social Security Fund (NSSF) is Kenya’s mandatory pension and social security scheme. Every formally employed Kenyan contributes a portion of their salary each month, and their employer matches it. The money is meant to provide a retirement benefit when you leave formal employment.

The NSSF Act 2013 — which replaced the old flat-rate KES 200/month contribution — introduced a tiered contribution system based on your salary. It also established a phased implementation over several years, with contribution levels increasing annually as the new system beds in.

We are now in Year 4 of that implementation, which began in February 2026.

NSSF Year 4 Rates 2026: The Exact Numbers

The NSSF contribution is calculated on two tiers:

Tier I covers earnings up to the Lower Earnings Limit (LEL). Tier II covers earnings between the LEL and the Upper Earnings Limit (UEL).

Year 4 rates effective February 2026:

| Amount | |

|---|---|

| Lower Earnings Limit (LEL) | KES 7,000 |

| Upper Earnings Limit (UEL) | KES 108,000 |

| Tier I contribution rate | 6% of LEL |

| Tier II contribution rate | 6% of earnings between LEL and UEL |

| Maximum employee contribution | KES 6,480/month |

| Maximum employer contribution | KES 6,480/month |

| Maximum total contribution | KES 12,960/month |

How Much Are You Actually Paying? Calculate Yours

Your NSSF contribution depends on your gross salary. Here is how to calculate it:

Step 1: Calculate Tier I contribution: 6% × KES 7,000 = KES 420

Step 2: Calculate Tier II contribution: 6% × (your gross salary − KES 7,000), subject to a maximum of 6% × (KES 108,000 − KES 7,000) = 6% × KES 101,000 = KES 6,060

Total maximum: KES 420 + KES 6,060 = KES 6,480

Real examples by salary:

| Gross Monthly Salary | NSSF Employee Contribution (Year 4) |

|---|---|

| KES 20,000 | KES 420 + KES 780 = KES 1,200 |

| KES 40,000 | KES 420 + KES 1,980 = KES 2,400 |

| KES 60,000 | KES 420 + KES 3,180 = KES 3,600 |

| KES 80,000 | KES 420 + KES 4,380 = KES 4,800 |

| KES 108,000 and above | KES 420 + KES 6,060 = KES 6,480 |

Your employer pays the same amount on top of your contribution.

How Year 4 Compares to Previous Years

To understand why your February payslip changed, here is the progression of NSSF contribution limits:

| Year | Upper Earnings Limit | Max Employee Contribution |

|---|---|---|

| Old flat rate (pre-2014) | — | KES 200/month |

| Year 1 (2014 implementation) | KES 18,000 | KES 1,080 |

| Year 2 | KES 36,000 | KES 2,160 |

| Year 3 | KES 72,000 | KES 4,320 |

| Year 4 (Feb 2026) | KES 108,000 | KES 6,480 |

If you earn KES 108,000 gross or more, your NSSF contribution jumped from KES 4,320 in Year 3 to KES 6,480 in Year 4 — an increase of KES 2,160/month.

At the KES 50,000 salary level, the jump was approximately KES 720/month more than Year 3.

How NSSF Affects Your Full Payslip in 2026

NSSF is just one of several mandatory deductions. To understand your full take-home pay, here is how all deductions stack up in 2026:

Mandatory deductions from gross salary:

- SHIF (Social Health Insurance Fund): 2.75% of gross salary (no cap, minimum KES 300)

- NSSF: Tiered as above (reduces taxable income)

- Affordable Housing Levy (AHL): 1.5% of gross salary

- PAYE income tax: Applied to taxable income after NSSF and SHIF deductions

Example: KES 80,000 gross salary in 2026

| Deduction | Amount |

|---|---|

| NSSF (employee, Year 4) | KES 4,800 |

| SHIF (2.75%) | KES 2,200 |

| Affordable Housing Levy (1.5%) | KES 1,200 |

| PAYE (on taxable income) | ~KES 11,000 |

| Total deductions | ~KES 19,200 |

| Approximate net take-home | ~KES 60,800 |

Note: NSSF and SHIF reduce your taxable income before PAYE is calculated. AHL does not reduce taxable income following the repeal of AHL tax relief in December 2024.

Is Your Employer Complying With Year 4 Rates?

Not all employers have updated their payroll systems correctly for Year 4 rates. Here is how to check:

Step 1: Look at your February 2026 payslip. Find the NSSF deduction line.

Step 2: Calculate what you should be paying based on your gross salary using the table above.

Step 3: If your payslip shows a lower amount than it should, your employer may not have updated their system.

What to do if your employer is underpaying: Non-compliance with NSSF rates is a legal issue for your employer, not you. However, underpayment means your NSSF account is not being credited correctly, which affects your eventual retirement benefit. Report to your HR department in writing and keep a copy for your records.

What Happens to Your NSSF Contributions?

Your NSSF contributions are invested by the NSSF Fund on your behalf. The fund invests in government securities, equities, real estate, and other assets.

Your contributions build up over your working life and become accessible when you:

- Reach age 60 (normal retirement)

- Reach age 50 and leave employment (early retirement)

- Become permanently incapacitated

- Emigrate permanently from Kenya

The total benefit is your accumulated contributions plus investment returns minus applicable fees.

Important: Your NSSF benefit is separate from any employer pension scheme or private retirement savings. Many Kenyans have both NSSF and a private pension — NSSF is the mandatory floor.

The Case For and Against NSSF

The case for:

- Your employer matches every shilling you contribute — that is an immediate 100% return on contribution

- Contributions reduce your PAYE taxable income, giving you a small immediate tax saving

- It creates forced retirement savings discipline

- Investment returns have historically been reasonable, though not spectacular

The case against:

- Returns on NSSF funds have historically lagged behind money market funds and T-Bills

- Access is locked until retirement age — it is completely illiquid

- NSSF has had governance and management controversies over the years

- Higher earners argue the contribution limit is too high relative to expected benefits

The honest answer: NSSF is mandatory for formally employed Kenyans — you cannot opt out. The employer match makes it worth contributing to. But it should not be your only retirement savings vehicle. Supplement it with a personal pension, SACCO contributions, or direct investments in money market funds and NSE stocks.

Self-Employed and Informal Sector Workers: What About You?

If you are self-employed, a freelancer, or work in the informal sector, NSSF contributions are technically voluntary — though the government has been making efforts to extend mandatory coverage.

Voluntary NSSF contributions follow the same rate structure. If you want to contribute voluntarily, you can register with NSSF directly and make contributions through M-Pesa or bank transfer.

However, for most self-employed Kenyans, the better retirement savings strategy is a combination of:

- A personal pension plan with a licensed provider (tax-deductible up to KES 30,000/month)

- SACCO membership

- Systematic investment in money market funds or T-Bills

Frequently Asked Questions

Can my employer deduct NSSF from my salary without telling me? NSSF deductions must appear as a line item on your payslip. You are entitled to see exactly how much is being deducted. If it is not shown, ask your HR department for a detailed payslip.

Does NSSF contribution count toward my retirement tax relief? Yes. NSSF contributions reduce your taxable income before PAYE is applied. This gives you a small tax saving each month.

What if I change jobs? Do I lose my NSSF contributions? No. Your NSSF contributions stay in your individual NSSF account regardless of where you work. When you join a new employer, provide your NSSF number so contributions continue into the same account.

Can I withdraw my NSSF before retirement? Only in specific circumstances: permanent incapacity, emigrating permanently from Kenya, or in some cases a partial withdrawal after age 50 if you have left formal employment. Early withdrawal for other reasons is generally not permitted.

Are NSSF contributions increasing further in Year 5? The NSSF Act 2013 set out the phased implementation schedule. Year 5 rates are expected to increase further, likely in early 2027. Watch for announcements from NSSF and KRA.

The Bottom Line

NSSF Year 4 rates represent a significant step up in mandatory pension contributions for most formally employed Kenyans. If you earn KES 108,000 or more, you are now contributing KES 6,480 per month — more than 30 times the old KES 200 flat rate.

The employer match is real value. The tax deduction helps. But NSSF alone will not fund a comfortable retirement. Use Year 4 as a prompt to look at your full retirement picture — are you saving enough beyond the mandatory minimum?

Check your February payslip, confirm the right amount is being deducted, and make sure your employer is compliant. Your future self depends on it.

NSSF rates and regulations described in this article reflect the NSSF Act 2013 phased implementation as of February 2026. Rates are subject to change. Verify current rates at nssf.or.ke and kra.go.ke.