Affordable Health Insurance in Kenya 2026: SHA vs Private Cover Compared

Affordable Health Insurance in Kenya 2026: You are now contributing more to SHA than you ever paid to NHIF. For a Kenyan earning KES 80,000, the SHIF deduction is over KES 2,200 per month — more than the old NHIF maximum of KES 1,700. The question every employed Kenyan is asking is the same: is this enough, or do I still need private health insurance on top?

The honest answer requires understanding what SHA actually covers versus what private insurance covers — including the gaps that matter most: which hospitals are on the network, what ward class you receive, which conditions have benefit limits, and where SHA runs out and you are paying out of pocket.

This guide makes that comparison in plain language, covers the most affordable private health insurance options in Kenya in 2026, and tells you exactly which combination makes financial sense at your income level.

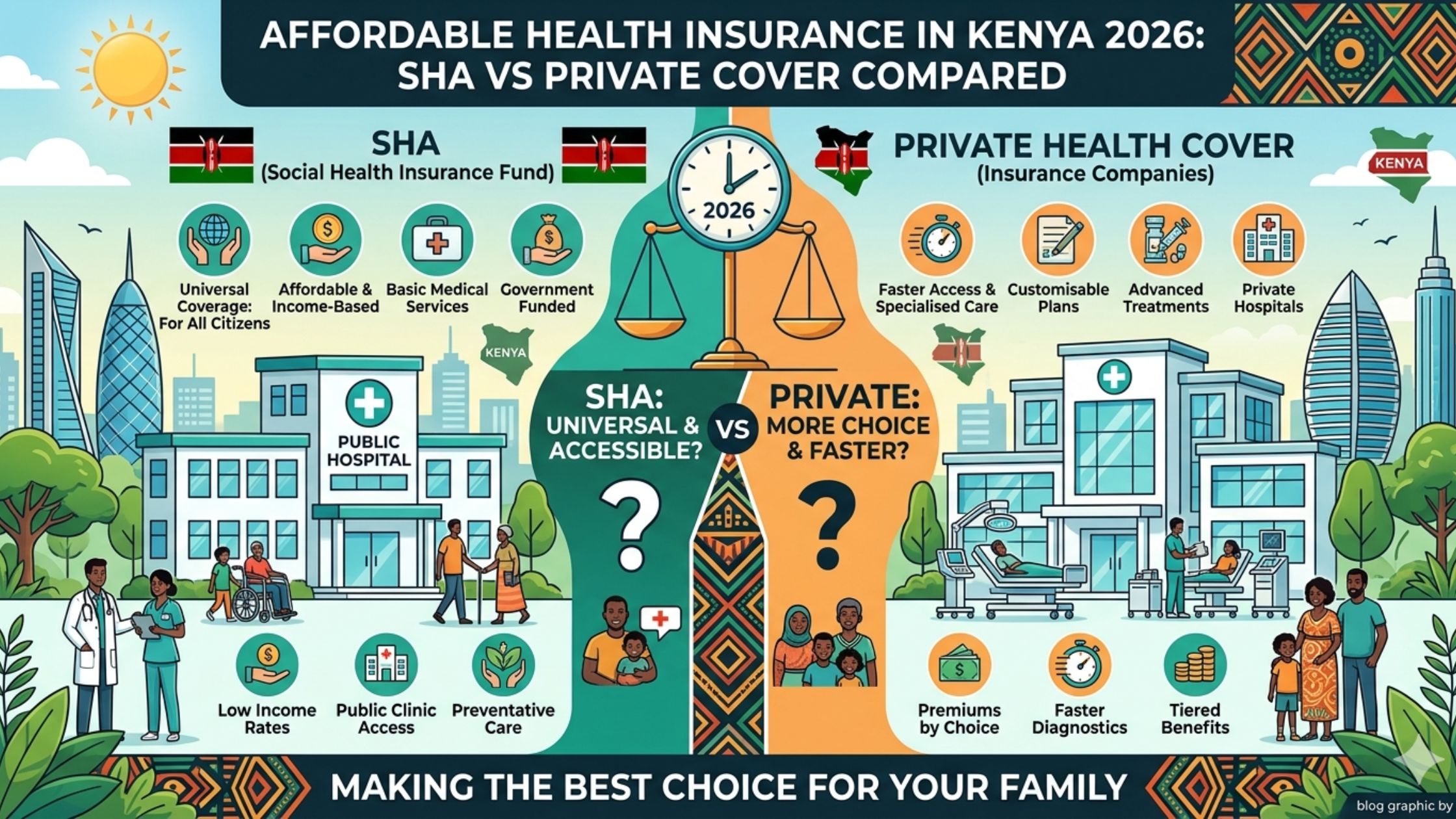

What SHA Actually Covers in 2026 — The Real Picture

Most Kenyans contributed to NHIF for years without fully understanding what it covered. SHA is more complex — three separate funds serving different purposes. Understanding them before comparing private insurance prevents you from paying for cover you already have or missing cover you need.

The Three SHA Funds

Fund 1 — Social Health Insurance Fund (SHIF) Funded by your 2.75% monthly payslip contribution. This is the main treatment fund. SHIF covers inpatient services at Level 4–6 public hospitals and accredited private hospitals — district hospitals, provincial general hospitals, national referral hospitals (Kenyatta, Moi), and a list of approved private facilities. Coverage includes inpatient care, surgery, maternity at accredited facilities, and specialist consultations within the network.

Fund 2 — Primary Healthcare Fund Covers Level 2 (dispensaries) and Level 3 (health centres) for all registered Kenyans — completely free, regardless of whether you have paid your SHIF contributions. Registration alone unlocks this benefit. If you need primary care at a dispensary or health centre, SHA Fund 2 covers it with no deduction from your SHIF balance.

Fund 3 — Emergency, Chronic and Critical Illness Fund The safety net for catastrophic health events — cancer treatment, organ failure, serious accidents, major surgery — when SHIF benefits are depleted. Has its own eligibility criteria and approval process. This fund exists because SHIF alone cannot cover the full cost of prolonged or highly complex treatment.

What SHA Does Not Cover Well — The Critical Gaps

SHA covers inpatient services fully in public hospitals and some accredited private hospitals but has limited outpatient and specialist care coverage compared to private insurance. Understanding the specific gaps determines whether private insurance makes sense for your situation.

Private ward accommodation. SHIF covers general ward hospitalisation. Semi-private and private rooms are out of pocket. In most Nairobi private hospitals, a private room costs KES 8,000–25,000 per night above the general ward rate.

Hospital network restrictions. SHA coverage applies only at SHA-accredited facilities. If you rely solely on SHA, you may have limited choices for hospitals and treatments. Some private hospitals preferred by middle-class Kenyans — Nairobi Hospital, Aga Khan, Karen Hospital — have partial or varying accreditation levels with SHA.

Dental and optical. SHA does not cover dental and optical care. Routine dental work, glasses, and optical consultations are entirely out of pocket under SHA.

Specialist outpatient beyond the formulary. SHA covers outpatient consultations at accredited facilities but specialist outpatient access in private settings is more limited than under a comprehensive private policy.

Chronic disease management. SHA provides limited coverage for chronic diseases in public hospitals, while private insurers often require additional coverage for these conditions. Kenyans managing diabetes, hypertension, or asthma who see private specialists regularly will find SHA’s chronic disease coverage insufficient for their needs.

The honest verdict on SHA alone: SHA provides genuine healthcare coverage for routine medical needs — primary care, general inpatient, maternity, and moderate-complexity hospitalisation at public facilities. It does not provide the level of coverage most Nairobi middle-class Kenyans expect when admitted to a private hospital or seeking specialist care. The gap is real and worth understanding clearly.

Do You Need Private Affordable Health Insurance on Top of SHA?

This is an honest framework — not designed to push you toward buying insurance you do not need.

You probably do NOT need additional private insurance if:

You earn under KES 40,000 per month — SHA covers the healthcare most likely to be needed at this income level, and private insurance premiums represent a proportionally large share of income that may be better directed toward savings or emergency funds.

You primarily use public hospitals — SHA works best at Level 4–6 public hospitals and dispensaries. If you are comfortable accessing care through the public system, SHA alone is adequate for most medical needs.

You have no dependants, or your family is fully covered through an employer group health scheme.

You probably DO need additional private insurance if:

You earn above KES 60,000 per month and expect private hospital admission when hospitalised — the ward class gap between SHA (general) and what you expect (semi-private or private) is real and significant.

You have school-age children with frequent medical needs — outpatient visits, specialist referrals, dental — that exceed SHA’s coverage.

You are self-employed with no employer healthcare contribution and you are paying all premiums yourself — your healthcare risk is entirely unmanaged beyond SHA.

You have a family member with a chronic condition requiring regular specialist visits and prescription management beyond SHA’s public facility formulary.

You specifically want access to Nairobi Hospital, Aga Khan, MP Shah, or Karen Hospital as your preferred treatment facilities.

Types of Private Affordable Health Insurance in Kenya

Understanding the product landscape prevents you from buying a comprehensive policy when a targeted one meets your need at a fraction of the cost.

Corporate/employer group health insurance is the best value health insurance available to any Kenyan. The employer pays part or all of the premium, and group rates are significantly lower than individual rates for equivalent coverage. If your employer offers a group scheme, enrol immediately — even if SHA covers the basics, employer group schemes almost always cover private hospitals, higher ward classes, and outpatient benefits that SHA does not.

Individual/family private health insurance is purchased directly from an insurer. Higher premiums than group schemes because there is no employer contribution and no group risk pooling. Provides genuine choice of hospital and ward class, outpatient coverage including specialist consultations, dental and optical benefits, and maternity coverage — all above what SHA provides.

Hospital cash plans pay a fixed daily cash benefit for each day of hospitalisation regardless of actual medical costs — typically KES 2,000–5,000 per day. Significantly cheaper than comprehensive insurance. Useful as a financial buffer against hospitalisation for people who cannot afford full private premiums but want some protection.

Critical illness cover pays a lump sum upon diagnosis of specific conditions — cancer, heart attack, stroke, kidney failure. Not the same as health insurance — it does not pay hospital bills directly but provides a lump sum that can fund treatment or replace lost income during recovery. High levels of dental and optical cover limits for individuals up to KSh. 50,000 each are available under comprehensive covers, and some plans provide long-acting family planning options.

Best Private Affordable Health Insurance in Kenya 2026

All providers listed here are licensed by the Insurance Regulatory Authority for 2026 — AAR Insurance Kenya, Britam General Insurance, CIC General Insurance, Jubilee Health Insurance, Madison General Insurance, Old Mutual General Insurance Kenya, and Sanlam Allianz General Insurance are all currently licensed to operate.

Jubilee Health Insurance — Best Overall Coverage

Jubilee Health Insurance is the largest insurance health insurance company in Kenya and controls 17% of the health insurance market share in Kenya.

- Individual annual premium: Approximately KES 18,000–45,000 depending on cover level and age

- Family of four (inpatient only): Starting from KES 51,000 for a family of four for inpatient cover

- Hospital network: Wide — including major private hospitals

- Outpatient cover: Available as an add-on to inpatient base

- Dental and optical: High levels of dental and optical cover limits for individuals up to KES 50,000 each

Jubilee CoverBora is specifically designed as an affordable entry-level plan — best for individuals only worried about emergencies.

Verdict: Best overall for breadth of coverage and hospital network. Jubilee Insurance has high scores for medical and group health claims — reputation for claims processing is strong. If you want one comprehensive plan from a market leader, Jubilee is the starting comparison point.

AAR Health Services — Best for Outpatient Integration

AAR Medical Insurance Company is among the top five biggest medical insurance companies in Kenya with a market share of 14%.

- Individual annual premium: Approximately KES 15,000–40,000

- Hospital network: Broad, including AAR’s own clinics for cost-effective outpatient

- Outpatient cover: Dental and optical included up to 10% of outpatient limit

- Maternity: Included in inpatient — no extra charge

- Unique feature: AAR insurance offers a no-claim discount from the third year as long as you don’t claim

AAR ShwAARi is the budget-focused product. AAR’s Shwaari starts paying in just seven days — one of the shortest waiting periods available. Designed with everyday Kenyans in mind and known for its strong network and responsive customer service.

Verdict: Strong outpatient integration through AAR’s clinic network. Best for families who regularly use AAR clinics for outpatient consultations. The no-claim discount rewards healthy families who use insurance as a safety net rather than routine care.

CIC Health Insurance (CIC Medisure) — Most Affordable Entry Level

CIC Insurance Group is popular among retail investors and cooperative sector employees for its cooperative backing.

- Individual annual premium: Approximately KES 12,000–35,000

- Hospital network: Solid national coverage

- SACCO integration: CIC’s cooperative roots make it particularly accessible for SACCO members

If you are part of a SACCO or cooperative, CIC Medisure is likely already on your radar.

Verdict: Most affordable entry level among reputable licensed providers. For SACCO members and cooperative sector employees, CIC’s products are often available at group rates through their SACCO — ask your SACCO secretary whether a CIC group health arrangement exists before buying individual cover.

Britam Health Insurance — Best Digital Experience

Britam has a strong reputation in digital claims management.

Britam structures their medical coverage into four main packages: Advantage (unrestricted hospital access, critical illness cover at top limits), Premier (similar hospital access, critical illness at specific limits), and Essential tiers with restricted hospital access.

Britam Bima Ya Mwananchi is the most affordable entry point. Premium starts from as low as KES 4,600 for individuals and KES 14,200 for a family of four. This is a micro-insurance product designed specifically for lower-income Kenyans — basic hospitalisation cover at a very low premium.

Britam Milele Health Cover targets the mid-market with comprehensive inpatient and outpatient options.

- Individual annual premium: KES 16,000–45,000 for Milele range

- Hospital network: Tier 2 and 3 for Essential plans; unrestricted for Advantage and Premier

Verdict: Best digital experience for claims and pre-authorisation. Britam offers a low budget cover (Bima Ya Mwananchi), a junior medical cover, a corporate cover, an SME cover, and a middle to high-income medical insurance cover — the widest product range of any Kenyan insurer. Start with Bima Ya Mwananchi if budget is the primary constraint; upgrade to Milele when income grows.

APA Insurance — Afya Nafuu (Best Overall Value)

APA Afya Nafuu is the best overall affordable health insurance in Kenya.

- Hospital access: Admits up to 75 years

- Cover: Comprehensive including chronic conditions

- Verdict: Packed with benefits especially for business owners and those who want full cover — worth comparing against Jubilee for comprehensive cover needs

Madison Betterlife — Best Family Budget Option

Madison Betterlife is best for hospital selection and a full-family solution on a budget.

- Good hospital panel selection

- Family-oriented pricing structure

- Verdict: Particularly worth considering for families prioritising specific hospital access at a manageable premium

Resolution Health (Part of Madison Group) — Best Inpatient-Only Product

Resolution Health focuses on flexible inpatient-only products that combine well with SHA for outpatient needs.

- Individual inpatient-only annual premium: Approximately KES 8,000–20,000

- What it covers: Hospitalisation, surgery, specialist inpatient care at private hospitals

- What it does not cover: Outpatient consultations (SHA covers these at public facilities)

Verdict: The most cost-effective private insurance product for the SHA era. Pair Resolution Health’s inpatient-only cover with SHA for outpatient — SHA handles dispensary and health centre visits free of charge, Resolution Health handles private hospital admission. Total premium significantly below a comprehensive standalone policy.

The Comparison Table

| Provider | Individual premium/year | Family (2+2)/year | Hospital network | Outpatient cover | Best for |

|---|---|---|---|---|---|

| APA Afya Nafuu | ~KES 15,000–40,000 | Confirm | Strong | Yes | Best overall value |

| Jubilee Health | ~KES 18,000–45,000 | From KES 51,000 (IP) | Widest | Add-on | Best market leader option |

| AAR ShwAARi | ~KES 15,000–40,000 | Confirm | Broad | Yes (10% of OP limit) | Best outpatient, short wait |

| Britam Milele | ~KES 16,000–45,000 | Confirm | Tier-based | Yes | Best digital experience |

| CIC Medisure | ~KES 12,000–35,000 | Confirm | National | Yes | Best for SACCO members |

| Madison Betterlife | Confirm | Budget-friendly | Good selection | Confirm | Best family budget |

| Resolution Health | ~KES 8,000–20,000 (IP only) | Confirm | Private hospitals | No (use SHA) | Best SHA top-up |

| Britam BYM | From KES 4,600 | From KES 14,200 | Basic | Basic | Most affordable entry |

Premiums are indicative and vary by age, cover level, and benefit limits. Request direct quotes from each insurer for accurate pricing.

The SHA Plus Private Insurance Combination That Makes Financial Sense

The optimal health coverage in Kenya in 2026 is not either/or. It is SHA for the baseline coverage you are already paying for, plus targeted private insurance that fills the specific gaps that matter for your situation.

The most cost-effective combination for most employed Kenyans:

SHA (mandatory, already deducted from payslip) covers: primary care at dispensaries (free), general ward inpatient at public hospitals, maternity at SHA-accredited facilities.

Add: An inpatient-only private policy — Resolution Health, Jubilee CoverBora, or AAR inpatient-only — at approximately KES 8,000–20,000 per year. This covers private ward accommodation, specific private hospitals, and hospitalisation costs above SHA’s benefit limits.

What this costs for someone earning KES 80,000 monthly:

- SHIF from payslip: KES 2,200/month = KES 26,400/year (already deducted, non-optional)

- Inpatient top-up: approximately KES 15,000/year

- Total annual health protection cost: approximately KES 41,400/year

What this delivers: Free primary care at dispensaries (SHA Fund 2), comprehensive general inpatient at public hospitals (SHIF), private ward access and preferred hospital for planned or emergency hospitalisation (top-up policy).

Compare this to: A standalone comprehensive private policy for a family of four costing KES 100,000–200,000 per year — providing largely duplicative coverage for outpatient that SHA already covers at public facilities. The SHA plus targeted top-up approach delivers most of the benefit at approximately one-third the cost.

The employer scheme advantage: If your employer provides group health insurance, the combination of that scheme plus SHA likely provides comprehensive coverage already. Before buying any individual insurance, check your employer scheme’s specific benefits — particularly which hospitals are covered, what ward class, and whether dental and optical are included. Many Kenyans pay for individual insurance that duplicates employer coverage they already have.

How to Buy Private Health Insurance in Kenya

Step 1: Determine what you actually need. Which hospitals do you want access to? What ward class — general, semi-private, or private? Is outpatient your priority or inpatient? How many family members need cover? Answering these questions before requesting quotes prevents buying a product misaligned with your needs.

Step 2: Get quotes from at least three providers. Jubilee (jubileehealth.co.ke), AAR (aarhealth.com), and Britam (ke.britam.com) all have online quotation tools. CIC has integrated insurance products through the MCo-op Cash app. APA Insurance through apainsurance.co.ke. Request quotes at the same cover level from each — inpatient limit, outpatient limit, family size — to make them comparable.

Step 3: Compare actual benefits, not just premium. Scan waiting periods — confirm how long you must wait for chronic, maternity, or surgery claims before calling a plan cheap. Pre-existing conditions waiting periods are typically 12 months, maternity waiting periods 10–12 months. The total cover limit should be at least three times what you pay annually as a quick value check.

Step 4: Check the hospital panel. Download the insurer’s approved hospital list and confirm your preferred facilities are included. Make sure your preferred Tier III hospitals are on the list. A policy that does not cover your preferred hospital is a policy you will regret on the day you need it.

Step 5: Check the claims process. How do you get pre-authorisation for hospitalisation? Is there a 24-hour line? A mobile app? The claims process experience matters more than the premium on the day you actually use the insurance.

Step 6: Pay annually if possible. Annual payment typically provides a small premium discount. Keep your policy certificate and insurer emergency number saved on your phone — you will need both for hospital admission.

Frequently Asked Questions – Affordable Health Insurance

Is SHA alone sufficient for a middle-class Kenyan family?

For routine medical needs — primary care, minor illness, general inpatient at public hospitals, maternity — yes. SHA provides comprehensive coverage for Kenyans accessing public healthcare facilities. For private hospital access, specific ward class preferences, dental, optical, or chronic disease management at private facilities, SHA alone is insufficient for middle-class expectations.

Does private health insurance cover pre-existing conditions?

Most policies impose a waiting period — typically 12 months — before pre-existing conditions are covered. Some insurers will impose waiting periods or require proof of stability for pre-existing conditions. AAR’s ShwAARi has one of the shortest waiting periods. Read the policy document carefully before buying if you have a pre-existing condition.

Can I claim on both SHA and private insurance for the same hospitalisation?

Yes — this is called co-insurance or coordination of benefits. SHA pays its portion first, and your private insurer covers costs above SHA’s payment or in facilities not covered by SHA. You cannot profit from double-claiming (claim more than the actual cost) but you can use both covers to minimise or eliminate out-of-pocket costs.

Is employer health insurance better than individual private insurance?

Almost always yes. Employer group schemes benefit from risk pooling across many employees, which significantly reduces the per-person premium. Employers also typically contribute part of the premium. The same coverage that costs KES 40,000 per year individually may cost KES 15,000–20,000 via an employer scheme with the employer paying the balance.

What is the cheapest health insurance in Kenya 2026?

Britam’s Bima Ya Mwananchi starts from as low as KES 4,600 for individuals — the lowest premium entry point from a major licensed insurer. For a slightly broader product, Jubilee CoverBora is the best option for individuals only worried about emergencies.

Does SHA cover dental and optical?

No. SHA does not cover dental and optical care. Any dental treatment or optical correction is fully out of pocket under SHA. Comprehensive private insurance policies typically include dental and optical up to annual sublimits — Jubilee offers up to KES 50,000 for each under comprehensive plans.

How do I register my family under SHA?

Register your family members via sha.go.ke or by dialling *147#. Adding a spouse requires uploading a marriage certificate or affidavit. Adding children requires a birth certificate or birth notification. See our NHIF vs SHA Kenya 2026 guide for the complete registration process.

The Bottom Line – Affordable Health Insurance in Kenya 2026

SHA is a genuine improvement over NHIF — better primary care access, dedicated catastrophic illness funding, and an income-proportional contribution that is fairer than the old flat-rate bands. Health insurance in Kenya has undergone a dramatic transformation from the monopoly of the National Hospital Insurance Fund to a mixed system featuring SHA, private medical insurance companies, and community-based health financing schemes.

For most Kenyans earning under KES 50,000 per month, SHA alone provides adequate coverage for routine needs. For Kenyans earning above KES 60,000 who expect private hospital access, an inpatient top-up policy at KES 8,000–20,000 per year per person bridges the gap between SHA’s general ward coverage and private care — at a fraction of the cost of standalone private insurance.

The worst outcome is having neither SHA registration nor private insurance. That is one unexpected hospitalisation away from a financial crisis that erodes years of savings. Register for SHA at *147# if you have not done so. Then assess whether your income and healthcare expectations require a targeted private top-up.

Insurance providers verified as IRA-licensed for 2026. Premium ranges are indicative — actual premiums vary by age, benefit limits, and insurer. Request direct quotes before purchasing. All providers mentioned are regulated by the Insurance Regulatory Authority of Kenya.

Related reading: