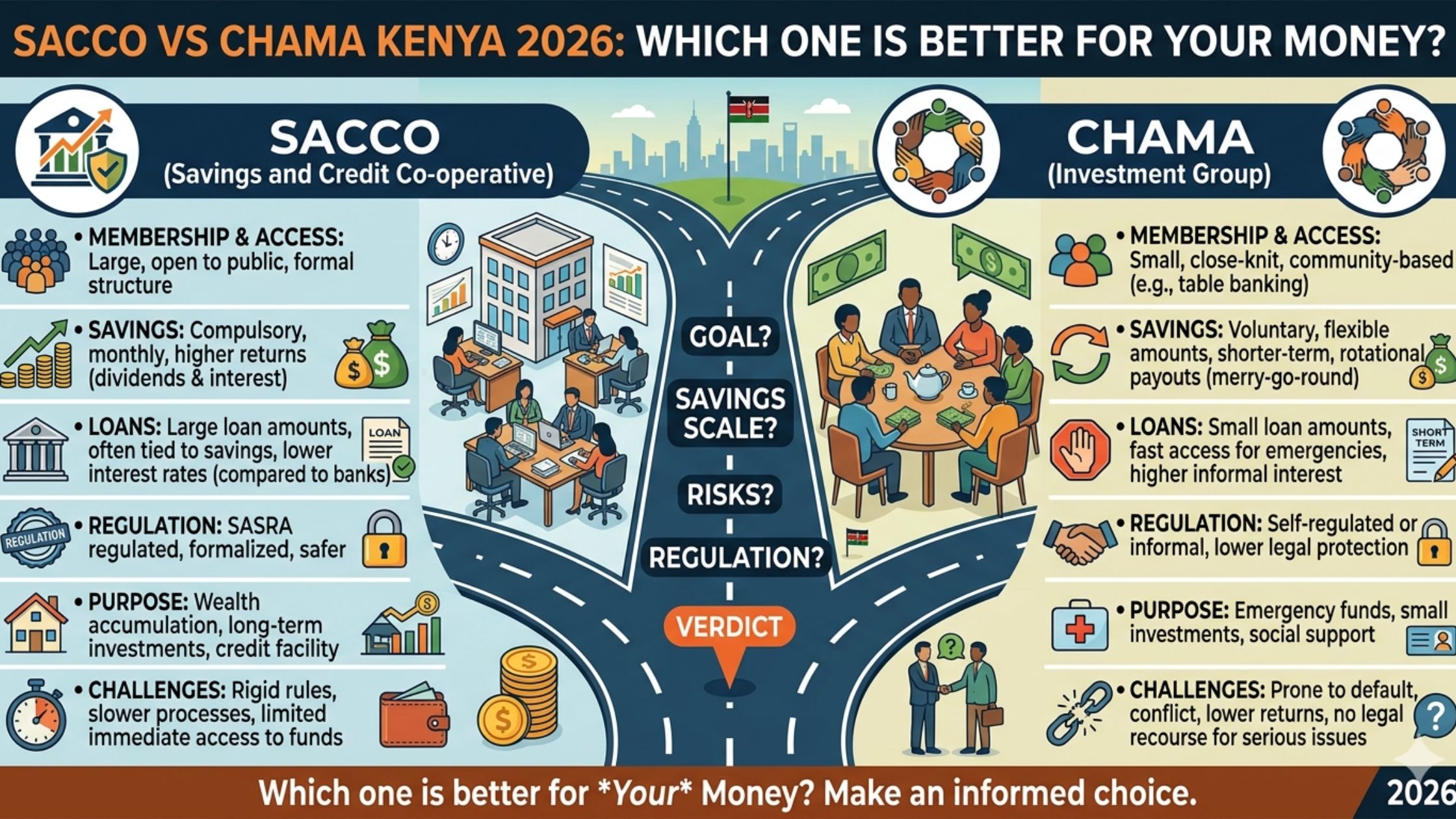

SACCO vs Chama Kenya 2026: Which One Is Better for Your Money?

SACCO vs Chama Kenya 2026 — it is a question that comes up in nearly every WhatsApp group where Kenyans are trying to grow their money together. Both have built real wealth for millions of people. Both have also disappointed people who did not understand what they were joining.

The honest answer is that they are not really competing products. They solve different problems. Understanding which one suits your situation — or whether you actually need both — can be the most important financial decision you make this year.

Last updated: April 2026 | Reading time: 7 minutes

Here is the clear, no-nonsense breakdown.

What Is a Chama? (And Why 300,000 of Them Exist in Kenya)

A chama is an informal savings and investment group. Members agree to meet regularly — weekly or monthly — pool money together, and either rotate the lump sum among themselves or invest it collectively.

There are an estimated 300,000 chamas in Kenya managing a combined KES 300 billion in assets. One in three Kenyans is a chama member. It is not a niche financial product — it is a national institution.

Chamas come in two main forms:

Merry-go-round (ROSCA): Each member contributes a fixed amount at each meeting. The total collected goes to one member on rotation. If ten members contribute KES 1,000 monthly, one person receives KES 10,000 each month. Simple, liquid, and widely practised.

Investment chama: Members pool contributions and invest collectively — in land, shares, rental property, a business, or a money market fund. Returns are shared or reinvested. This is where chamas start to look like serious wealth vehicles.

What makes a chama work is social accountability. You know every person in the group. Missing a contribution is not a form to fill — it is a conversation with people who know your name and your situation. For many Kenyans, this social pressure is more effective than any formal savings mechanism.

What Is a SACCO? (The Regulated Alternative)

A SACCO (Savings and Credit Cooperative Organisation) is a formally registered financial institution that operates like a cooperative bank. Members pool savings, earn dividends on their share capital, and access loans at rates far below commercial banks.

Kenya has over 14,000 registered SACCOs. The largest — Mwalimu National — holds over KES 100 billion in assets and serves 90,000+ teachers. They are regulated by SASRA (Sacco Societies Regulatory Authority), which means regular audits, capital requirements, and consumer protection mechanisms that informal chamas simply do not have.

The primary reason most Kenyans join a SACCO is not the dividend — it is access to affordable loans. A SACCO loan at 1% per month (12% annually) compared to a mobile loan at 7.5% per month (90% annually) is not a small difference. It is the difference between a loan that helps you build something and one that traps you in a cycle of debt.

SACCO vs Chama: The Side-by-Side Comparison

| Factor | SACCO | Chama |

|---|---|---|

| Regulation | SASRA-regulated (formal) | Informal (no regulator) |

| Minimum to join | KES 1,000–10,000 shares | Whatever the group agrees |

| Loan access | Yes — up to 3–5X savings at 1%/month | Depends on group; often 5–20%/month |

| Dividend/returns | 8–13% annually on share capital | Depends entirely on investment chosen |

| Liquidity | Low — shares locked | Flexible — group decides rules |

| Safety | Deposit Guarantee Fund up to KES 100K | No formal protection |

| Social accountability | Formal (payroll deduction, contracts) | High (personal relationships) |

| Control | Democratic — member votes at AGM | Group rules — can be flexible or chaotic |

| Transparency | Audited accounts published | Depends on how well records are kept |

| Who can join | Employed, self-employed (varies) | Anyone the group accepts |

| Best for | Long-term savings + cheap loans | Pooled investment + social wealth building |

Where Chamas Win

Flexibility that SACCOs cannot match. A chama can decide overnight to invest in land in Nakuru, buy shares in a company, or pivot to a different strategy entirely. A SACCO has a defined mandate, regulatory requirements, and board approval processes. Chamas move at the speed of a WhatsApp decision.

Collective investment power. Ten people each contributing KES 5,000 per month have KES 600,000 per year to deploy. That is enough to buy a plot in a satellite town, fund a small commercial development, or build a meaningful NSE portfolio. No individual member could do this alone — but the chama can.

No employment requirement. SACCOs — especially the best-performing ones like Mwalimu and Stima — are restricted to specific employment sectors. Chamas accept anyone the group trusts. A market trader, a boda boda operator, and a nurse can be in the same chama with no paperwork required.

The social dimension. Chama meetings are also community. Financial discipline is enforced through relationships, not contracts. For many Kenyans, this human accountability is more motivating than any formal system. Some of Kenya’s most successful businesswomen built their capital through chamas before they ever opened a bank account.

Where SACCOs Win

Loan rates that chamas simply cannot beat. Most chamas that offer loans charge 5%–20% per month — partly to cover the risk of lending within a group of people you know personally. SACCOs charge 1%–1.5% per month because they are properly capitalised, regulated institutions. On a KES 200,000 loan over 12 months, the difference between 1% and 10% per month is over KES 200,000 in interest. That is not a rounding error — it is a life-changing difference.

Regulatory protection. When a chama collapses — and some do, usually through mismanagement or betrayal by a trusted member — there is no SASRA to call, no deposit insurance, and no auditor’s trail. Your money is gone and your only recourse is small claims court or a personal confrontation. SASRA-regulated SACCOs carry formal consumer protections including a Deposit Guarantee Fund that covers deposits up to KES 100,000.

Payroll deduction discipline. For employed Kenyans, SACCO contributions deducted directly from salary before it hits your account is the most powerful savings mechanism available. You never see the money, so you never spend it. Most chama members transfer manually — and some months, life happens.

Scale of financial services. Large SACCOs offer mortgages, development loans of up to KES 10 million, school fees products, and emergency loans processed within 48 hours. A chama — no matter how well-run — cannot replicate this range of services.

The Three Most Common Mistakes People Make Choosing Between Them

Mistake 1: Joining a chama thinking it has SACCO-level safety. A chama run by your friends is not a regulated financial institution. If the chairperson runs off with the money, your options are limited. Always ensure your chama has: a proper constitution signed by all members, a bank account that requires two signatories, clear minutes of every meeting, and annual financial statements reviewed by a neutral party.

Mistake 2: Joining a SACCO only for the dividend and ignoring the loan product. The dividend is attractive, but the real wealth-building tool in a SACCO is the loan. A member who builds KES 200,000 in share capital and uses it to access a KES 600,000 loan at 1% per month — to buy land, renovate a rental unit, or fund a business — grows wealth far faster than one who simply collects the annual dividend.

Mistake 3: Treating them as alternatives rather than complements. The smartest financial strategy many Kenyans use is both — a SACCO for the loan access and forced savings discipline, and a chama for collective investment in specific opportunities (land, shares, real estate) that the SACCO’s structure does not support.

Which One Is Right for You?

Join a SACCO if:

- You are employed and want payroll deduction savings

- You need access to an affordable loan in the next 1–3 years

- You want regulated, audited safety for your savings

- You are building toward a mortgage, land purchase, or business loan

Join a Chama if:

- You want to pool resources for a collective investment (property, shares, business)

- You want flexibility in investment decisions

- You are self-employed and not eligible for sector-specific SACCOs

- The social accountability of a group setting works better for your savings discipline

Join both if:

- You are employed, can afford both contributions, and want the safety of SACCO loans alongside the investment upside of a well-run chama

- This is the approach most financially successful Kenyans quietly use

How to Make a Chama Safe — The Non-Negotiables

If you are in a chama or starting one, these are not optional:

Write a constitution. Every chama needs documented rules covering contributions, loans (if offered), exit procedures, and dispute resolution. Chamasoft offers free templates.

Open a group bank account requiring two signatories. Never let one person control the money.

Keep written minutes of every meeting, signed by all attendees. This is your paper trail if things go wrong.

Agree on an investment strategy in writing before pooling money. “We will invest in land in Ruiru” is not a strategy. “We will buy a plot not exceeding KES 500,000 in Ruiru ward by December 2026, approved by unanimous vote” is a strategy.

Conduct annual financial reviews. Even informally — a member with accounting experience can prepare a one-page summary of contributions, investments, and balances.

The Bottom Line

A SACCO is a regulated financial institution that protects your savings and gives you cheap loans. A chama is a community savings vehicle that gives you collective investment power and flexibility. Neither is universally better — but understanding what each does well means you can use both intelligently rather than choosing between them.

In 2026 Kenya, the question is not SACCO vs Chama. It is: which combination of both fits where you are financially right now?

This article is for informational purposes only and does not constitute financial advice. Verify SACCO licensing at sasra.go.ke before joining any SACCO. Sources: SASRA Kenya, Wikipedia Chama research, Cytonn Investments, Fibo360 Kenya.